Business to Business (B2B) purchases, just because you are not charged VAT by a non-Irish Supplier, this does not mean that you don’t have to pay or record vat on EU and Non-EU imports.

The VAT 3 Return and the RTD form require you to record VAT you did not have to pay out but are liable to pay. Did you know you have a liability to pay VAT on EU imports?

A brief history of VAT at Point of Entry

Before the European Union Single Market, every time a business imported goods into Ireland from an EU or Non-EU country, that business had to pay VAT at point of Entry. This meant before you could get the goods to your premises you had to pay the Revenue Commissioners Customs and Excise Section, both the VAT and Duty that was deemed payable on the goods you were importing into Ireland.

What is a point of entry?

The point of entry into Ireland is usually a Ship Port, an Airport or a land border crossing check point.

How is VAT at point of Entry calculated?

Every item has a VAT rate assigned to it

In simple terms, what VAT rate would an Irish supplier charge you if you bought the goods from them, then that is the VAT rate the VAT at point of entry would be calculated at. VAT is charged on the Customs Value of the goods

Example of Vat at point of entry calculation and customs valuation of goods (Non-EU purchases)

Goods imported and invoiced in US Dollars (simplified version)

| Goods imported value in US Dollars | USD | 12,000.00 |

| Costs of Shipping Goods to Ireland | USD | 1,000.00 |

| Custom Value | USD | 13,000.00 |

| Duty on goods @ 5% | USD | 650.00 |

| Total Customs Value in US Dollars | USD | 13,650.00 |

| Total in EURO @ exchange rate of 1.15 | EUR | 11,869.57 |

| Vat at 23% on Total Customs Value | EUR | 2,730.00 |

Note 1: The US Dollar exchange rate is the rate the Customs and Excise section set, not the rate you pay for your US Dollars.

Note 2: There are other schemes available for VAT at point of entry e.g. deferred and section 56

In this case the Vat at Point of Entry payable is €2,730

To have your goods released from the ship port or airport to be delivered to your premises, you would have to pay the VAT and Duty amounts calculated on your imported goods.

You can claim this VAT back on your VAT 3 return as a deduction just like any vat amount charged by an Irish supplier on their invoice.

Current Rules for Non-EU imports

VAT at point of entry is still due to be paid when you import goods, but you can now postpone paying the VAT at point of entry. This is a scheme that commenced in January 2021.

This means that you still owe the VAT, but you don’t have to pay it immediately at the point of entry. You can now but instead declare it on your VAT 3 return as both a liability and a deduction with a net cash cost to your business of Zero. This is very good for your business cash flow as you do not have to immediately pay over the VAT amount to get your goods.

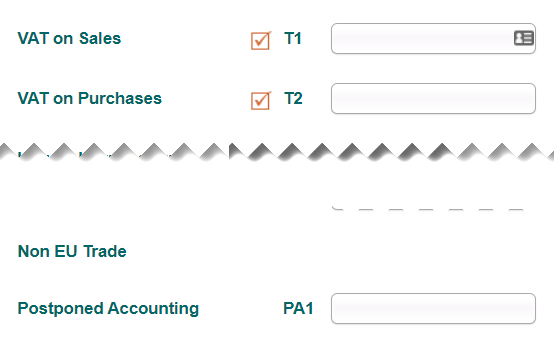

The administration of the Vat at point of entry on the VAT 3 return is that,

in the T1 box you include the Vat at point of entry with the vat on sales values for the T1 box and

in the T2 box you also include the Vat at point of entry with the vat on purchases value

The net result is a Zero amount

In the PA1 box you enter the net amount of the goods you processed through the Postponed Accounting scheme.

If you don’t document the postponed VAT correctly, you will have filed an incorrect VAT 3 return. When you go to complete the RTD form (Return of Trading Details) showing all the net values, it won’t agree to the VAT 3 return.

Current Rules for EU imports

If your business is VAT registered on Ireland and you supply that VAT number to your EU supplier, they do not have to charge you VAT. But you are still liable to pay the VAT at point of entry for those goods. Because the EU has a single market, no import documentation is required, and those EU imports are not held up by the Revenue Commissioners Customs and Excise section at the ship port or Airport and can be delivered directly to your premises.

There is no duty on goods imported from EU countries.

What you and your business must do is to use the process of self accounting for the VAT you did not pay on these EU imports.

Here is what the Revenue Commissioners web site has to say about EU imports / intra-Community supply (ICS)

Under this system:

- the supply is zero-rated in the Member State of dispatch as an ICS.

- the purchaser is liable for VAT on the acquisition of the goods.

- the purchaser must account for the VAT in their VAT return. The rate applicable is the rate of VAT which applies in their own Member State.

- if they are entitled to an input credit for the VAT payable on the ICA, this is reclaimed in the same VAT return

- and

- the purchaser must account for VAT on any subsequent supply of the goods.

Example of Vat (Self Accounting) calculation and customs valuation of goods

Goods imported and invoiced in Euro

| Goods imported from Germany (invoice value) | EUR | 12,000.00 |

| Total Customs Value | EUR | 12,000.00 |

| Vat at 23% on Total Customs Value | EUR | 2,760.00 |

How to account for EU VAT in your VAT 3 return

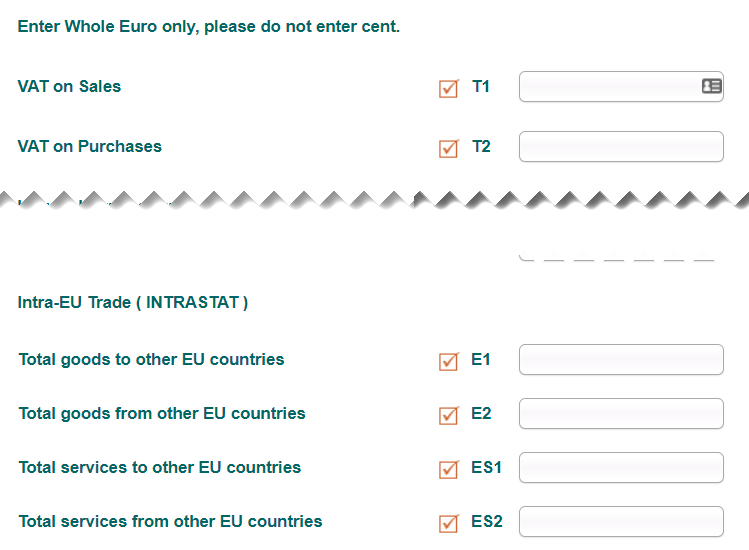

The administration of the Vat (Self Accounting) on the VAT 3 return is that,

in the T1 box you include the Vat that would have been charged by an Irish supplier with the vat on sales values for the T1 box and

in the T2 box you also include the Vat that would have been charged by an Irish supplier with the vat on purchases value

The net result is a Zero amount value

In the E1 and E2 boxes you enter the net value of the goods or services that are EU imports

Extract from VAT 3 Return

If you don’t document the EU Imports correctly, you will have filed an incorrect VAT 3 return. When you go to complete the RTD form (Return of Trading Details) showing all the net values, it won’t agree to the VAT 3 return.